Sole Trader vs Limited Company UK: Which Business Structure Is Right for You?

When you are starting a business in the UK, one of the most important decisions you will make is choosing the right legal structure. The debate around sole trader vs limited company UK affects everything from how much tax you pay to how much personal risk you carry. Get it wrong and you could end up overpaying tax, facing unnecessary liability, or creating paperwork you are not ready for.

This guide explains both structures in plain English, compares them side by side, and helps you decide which is the better fit for your situation whether you are a freelancer, a startup founder, or an entrepreneur relocating to the UK from abroad.

At its simplest, a sole trader and their business are the same legal entity. A limited company is a separate legal entity from the person who owns and runs it. That single distinction drives most of the differences in tax, liability, and administration between the two structures.

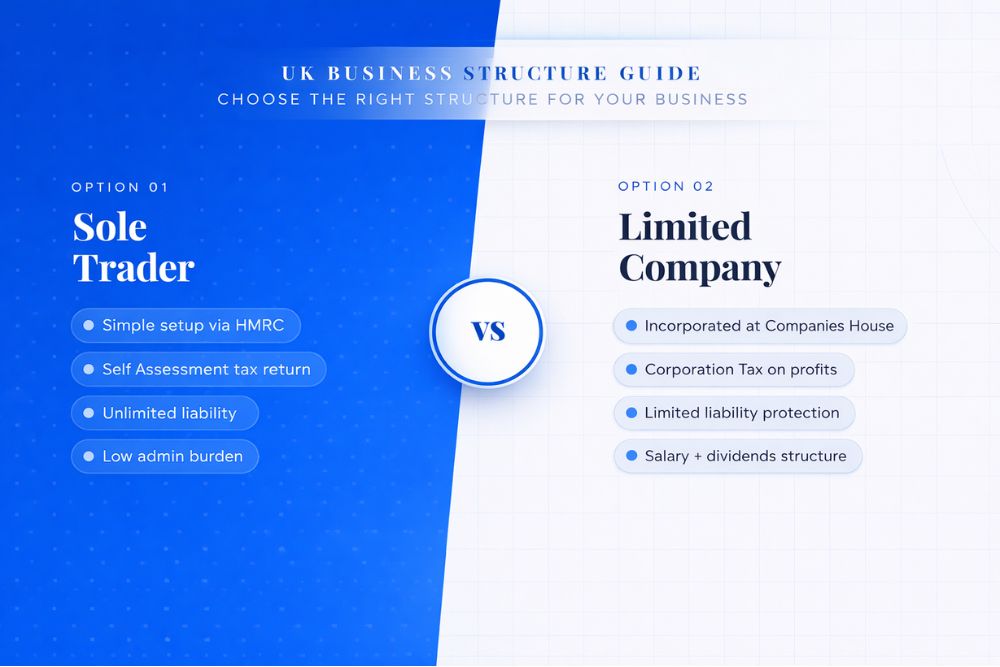

A sole trader is a self-employed individual who runs a business in their own name. It is the simplest and most common business structure in the UK.

To register as a sole trader UK, you notify HMRC that you are self-employed and complete a Self Assessment tax return each year. There is no registration fee and no requirement to file accounts at Companies House.

Key characteristics of a sole trader:

A sole trader is well-suited to individuals just starting out, those testing a business idea, or self-employed professionals such as consultants, tradespeople, and creatives with modest annual income.

A limited company is a distinct legal entity registered at Companies House. The most common type is a private limited company (Ltd). When you incorporate a company in the UK, you create a business that can own assets, enter contracts, and take on liabilities in its own name entirely separate from you as the director or shareholder.

Key characteristics of a limited company:

A limited company requires more administration, but it offers important protections and can be more tax-efficient once profits reach a certain level.

| Feature | Sole Trader | Limited Company |

| Legal status | Same as the owner | Separate legal entity |

| Personal liability | Unlimited | Limited to share value |

| Setup process | Register with HMRC only | Incorporate via Companies House |

| Setup cost | Free | From £12 online |

| Tax paid on profits | Income Tax + NI via Self Assessment | Corporation Tax (currently 19–25%) |

| Salary flexibility | No — all profit is personal income | Yes — salary plus dividends |

| Privacy | Name is public; finances are not filed | Annual accounts filed publicly |

| Credibility | Lower in some sectors | Generally perceived as more professional |

| Administrative burden | Low | Moderate to high |

| Access to investment | Limited | Easier — shares can be issued |

Understanding sole trader tax UK versus limited company tax UK is essential before you decide.

As a sole trader, your business profits are treated as personal income. You pay Income Tax at the basic rate (20%), higher rate (40%), or additional rate (45%) depending on how much you earn, plus Class 2 and Class 4 National Insurance contributions. There is no separation between business income and personal income.

A limited company pays Corporation Tax on its profits. The rate depends on how much profit the company makes smaller profits attract a lower rate. As a director-shareholder, you can take a modest salary (often set around the National Insurance threshold) and draw the remainder as dividends. Dividend income is taxed at lower rates than salary income through the dividend tax UK system, which can result in a lower overall tax bill compared to operating as a sole trader at higher income levels.

However, the tax advantage narrows when you factor in the additional accountancy costs a limited company typically requires. Always take advice from a qualified accountant before making assumptions about your personal tax position, as individual circumstances vary significantly.

Business liability UK is one of the most misunderstood areas for new business owners.

As a sole trader, you are personally liable for every debt and legal claim against your business. If your business cannot pay a supplier or loses a legal dispute, your personal savings, home, and assets could be at risk. This is a significant concern for businesses that hold contracts, employ staff, or work in sectors where claims are common.

A limited company protects you through the principle of limited liability. If the company fails, creditors can only pursue the company’s assets not your personal ones provided you have acted lawfully and not personally guaranteed any debts. This makes the limited company structure considerably safer for businesses that carry financial or legal risk.

Many limited company owners use an accountant to manage these obligations, which is an added ongoing cost to factor into your decision.

If you are a freelancer just starting out perhaps a designer, writer, developer, or consultant registering as a sole trader is usually the quickest and most practical first step. It allows you to begin trading immediately with very little paperwork, and it suits those earning under a certain threshold where the tax advantage of a limited company does not yet justify the extra cost and complexity.

That said, many freelancers move to a limited company once their earnings grow, or when clients particularly larger organisations prefer to work with an incorporated business. In sectors such as IT contracting, operating through a limited company is standard practice.

For entrepreneurs with growth plans, the self-employed vs limited company question often resolves in favour of the limited company. If you intend to bring in investors, take on employees, apply for business credit, or build a brand with long-term commercial value, a limited company is the more appropriate vehicle.

The startup business structure you choose also sends a signal to the market. A registered limited company tends to command more credibility with corporate clients, public sector buyers, and overseas partners. For Indian entrepreneurs starting a business in the UK specifically, a limited company is often preferable because it clearly separates UK business activity from personal affairs, makes it easier to open a business bank account, and provides a formal structure that supports future growth.

Staying a sole trader for too long. Many business owners delay incorporating even when their income justifies a limited company structure. The longer you wait, the more potential tax efficiency you may be missing.

Incorporating too early. Setting up a limited company before you have consistent income means you are paying for accountancy services and filing obligations that may not yet be worthwhile.

Confusing business and personal finances. This is common with sole traders but even more problematic if you run a limited company the company’s money is not your money until you formally pay it to yourself.

Ignoring VAT. Both sole traders and limited companies must register for VAT once turnover crosses the relevant threshold. Check the current HMRC registration rules and do not assume you are exempt.

Not taking professional advice. The sole trader vs limited company UK decision is not one-size-fits-all. A good accountant will assess your specific situation, income level, sector, and goals before making a recommendation.

The sole trader vs limited company UK decision is one of the most consequential choices you will make as a business owner, and there is no universally correct answer. Sole trader status is simple, low-cost, and well-suited to those starting out or earning modest income. A limited company offers liability protection, greater tax planning options at higher income levels, and stronger credibility in many markets.

As a general guide: if you are testing an idea or earning below around £30,000 to £35,000 in profit, starting as a sole trader is often the sensible choice. If your profits are growing, you face business risk, or you want to build something scalable, incorporating a company in the UK deserves serious consideration.

Whatever you decide, speak with a qualified UK accountant or business adviser before committing. Your personal circumstances including your income level, sector, risk exposure, and long-term plans should drive the decision.

Which is cheaper to set up a sole trader or a limited company? Registering as a sole trader is free. Incorporating a limited company costs from £12 online via Companies House, though ongoing accountancy fees make limited companies more expensive to run.

Which structure pays less tax? Limited companies can be more tax-efficient at higher profit levels due to Corporation Tax rates and the ability to pay dividends, but this depends on your individual circumstances always consult an accountant.

Can I switch from sole trader to limited company later? Yes. Many business owners start as sole traders and incorporate when their income grows. The process involves registering a new company and transferring your business activities to it.

Is a limited company safer than being a sole trader? Yes, in terms of personal financial risk. A limited company provides limited liability, meaning your personal assets are generally protected if the business fails provided you have acted lawfully.

What about VAT does it apply to both structures? Yes. Both sole traders and limited companies must register for VAT once turnover exceeds the current HMRC threshold, regardless of business structure. Check HMRC’s website for the latest figure.

Disclaimer: This article is for general informational purposes only and does not constitute legal or financial advice. Tax rules and thresholds change always consult a qualified UK accountant or adviser for guidance specific to your situation.